A guest blog from Jeb Brugmann: A Greek Tragedy in 6 Parts OR How northern Europe (also) avoids its systemic problems

1. IT STARTED AS A

POLITICAL PROJECT, aimed at eliminating European nationalistic tendencies and

ensconcing a single common market. All the parties involved were aware, if

not also complicit, that the 'numbers' were being cooked to support the

political project. To build Eurozone membership in the 1990s and early Aughts,

creative national accounting was used to meet financial thresholds

for entry (e.g.,3% deficit/GDP threshold). European statistical

and financial institutions knew that the fiscal household in a number of

countries was in poor condition, but chose to look the other way on Greece,

Spain, Portugal and Italy. Germany and France themselves violated the 3%

threshold in years leading up to the 2007+ global financial crisis (GFC). These

facts are overlooked amidst today's theatre of self-righteous northern

European finger-wagging towards Greece.

Meanwhile, the

European financial institutions (and the IMF) have continued to cooked numbers

to promote their failed austerity policies for Greece (see below).

The bail-out troika's unreality about the effectiveness of

austerity politics

2. THE EUROZONE WAS

BUILT UPON A FOUNDATION OF WILD WEST FINANCE. In the same era as the Euro

project, the deregulated banking sectors of the U.S. and Europe became

masters of high-risk/high-profit derivative instruments, involving shell games

of risk transfer and the purposeful obfuscation of financial realities and

integrity. A well known case in point is Goldman Sachs' 2001, 2.8

billion euro debt swap with Greece--which included a currency swap allowing

Greece to reduce the level of debt reported to Eurostat. “The Goldman Sachs

deal is a very sexy story between two sinners,” said Christoforis Sardelis, who

oversaw the swap as head of Greece’s Public Debt Management Agency from 1999

through 2004. German and French banks went on to make major loans to the corrupted,

clientilistic Greek governments of both the traditional right and left. They

knew that Greece's finances were a shaky house of cards, but felt protected by

the strength of the euro and the complicit support of northern European

governments and European institutions. Then the financial crisis hit--due

to the now famous collateralized debt obligation (CDO) derivatives of the U.S.

housing market (which had fueled a housing market that was building 60% more

housing than the growth in the number of actual U.S. households)--highlighting

the fact: it's a systemic problem, not a single-nation problem...

3. TRAGEDIES OFTEN

INVOLVE A FORK IN THE ROAD DECISION. The northern European

governments and the

European Union opted to bail out their risk-taking lenders instead of making

them pay for their failed and irresponsible lending practices. To do so, they

provided loans to Greece, Portugal, Spain and others to be flowed-through

to the lending institutions. The lenders took a bit of haircut but effectively

got bailed out. Meanwhile, fiscal austerity measures were imposed as loan

conditions, on the heals of the GFC recession itself...thus driving these

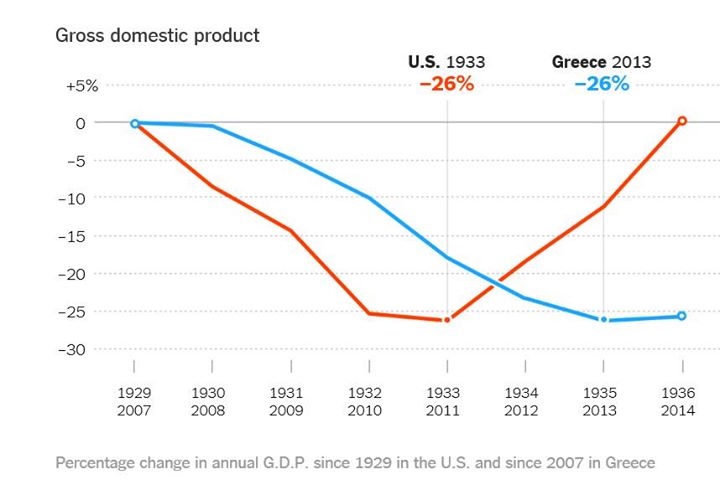

economies into depressions. In Greece, the decline in GDP has fallen further

and for a longer period than during the 1930s Great Depression in the

United States. (It took the opposite of austerity--protracted stimulus and then

wartime spending--to get the U.S. out of those depths.)

Post-GFC Greek economy under EU austerity (Source: New York

Times July 11)

Fiscal stimulus was

used in Germany, France, the U.S. and elsewhere to recover from the GFC...It

worked in Germany.

"Fiscal Stimulus in Germany in the Aftermath of the Great

Recession" (Gyorgy Barabas 2013) Y-axis = billions GDP in Euros

Somehow finance

ministries of certain countries find this to be an irresponsible option for

Greece. Now they add a fire sale of national assets. What odds of recovery do

London bookies give the latest scheme?

5. GREEK

TRAGEDIES CAN ONLY BE AVOIDED THROUGH SYSTEMIC CHANGE...Moral hazard in

the financial system has only been increased since the GFC. And it rests more

with the system's creditors than with its debtors. That seems to be

something much of the current northern European group of leaders still lacks

the spine to address. They are more prepared to provide 'humanitarian

assistance' for a deepening human crises on the continent than to muster this

courage.

6. IS THE EUROPEAN

POLITICAL PROJECT ITSELF NOW AT RISK? The last months' negotiations on the

Greek debt crisis have evidenced increasing nationalistic sentiments, with

classic utterances and tones of national-moral superiority, amongst

both northern European political leaders and the populace. They are joined

in self-righteousness by spokespeople from the finance industry. The

hypocrisies and lapses in recent historical memory are breathtaking. What

further tragedies remain in store?

Jeb Brugmann's latest book is

Comments

Post a Comment